Imagine finding a way to purchase your favorite stock – let’s call it Stock S – not at its market price but at a discount. This isn’t about waiting for a market dip; it’s about using options strategically to create what’s known as a “synthetic” position. To understand this, we’ll explore a principle called put-call parity.

How do synthetics work?

Put-call parity is a principle in options trading that establishes a relationship between the price of call and put options with the same strike price and expiration date. By buying a call option (\(C\)) and selling a put option (\(P\)) at the same strike, you can emulate owning the actual stock. If Stock S increases by 1%, the value of your combined options position (\(C – P\)) does too.

Why opt for a synthetic position over simply buying the stock? It comes down to the costs involved, specifically the ‘borrow rate’ (\(q\)), which is what you pay to borrow shares, usually for short selling. Market makers include this rate when pricing options. If the following condition is met:

\(e^{r} \times K<e^{q} \times S \)

then the synthetic position is effectively trading at a discount compared to buying the stock outright. Here, \(r\) is the risk-free interest rate, \(q\) is the borrow rate, \(S\) is the stock price, and \(K\) is the strike price. Let’s examine two examples to illustrate this:

Assume Stock S is trading at \( S = \$100 \) and the interest rate is 5% (\( r = 0.05 \)), while the borrow rate is at 10% (\( q = 0.10 \)).

Case 1

Suppose you’ve decided to strike at a price of \( K=\$100 \) with an option that expires in one year (\( T=1 \) year). Your strategy involves buying a call option (\( C \)) and selling a put option (\( P \)), both with a strike price of \( K=\$100 \) and a one-year expiration (\( T=1 \)). We’ll simplify the scenario by assuming there’s no dividend (\( D=\$0 \)).

\( (S – K) + K \cdot e^{rT} – S \cdot e^{-qT} + D\)

By substituting the values where \( S=\$100 \), the risk-free interest rate \( r=0.05 \), and the cost of carry \( q=0.10 \), we arrive at the equation:

\(100 – 100 + 100 \cdot e^{0.05} – 100 \cdot e^{-0.10} + 0= -\$5.38 \)

This calculation reveals that you effectively get a discount of \( \$5.38 \) on the synthetic position, which corresponds closely to the 5% differential between the borrowing rate (\( q \)) and the risk-free interest rate (\( r \)), based on the \( \$100 \) stock price.

If the stock \( S \) appreciates by 10% before expiration, a direct purchase of the stock would result in a \( \$10 \) profit from the increase. However, with the synthetic position, you capture both the \( \$10 \) gain from the call option due to the stock’s increase, plus the initial \( \$5.38 \) discount. This advantage highlights the potency of synthetic positions in options trading by enhancing your total profit from the transaction.

Case 2

Suppose you’ve decided to choose a strike price of \( K = \$50 \) while the stock price is \( S = \$100 \) with a one-year expiry (\( T=1 \)) and a dividend of \( D=\$1 \). The net cost after buying a call option (\( C \)) and selling a put option (\( P \)) is calculated as follows:

\( (S – K) + K \cdot e^{rT} – S \cdot e^{-qT} + D \)

By suBy substituting the values where \( S=\$100 \), the risk-free interest rate \( r=0.05 \), and the cost of carry \( q=0.10 \), we arrive at the equation:

\( 100 – 50 + 50 \cdot e^{0.05} – 100 \cdot e^{-0.10} + 1= \$43.04 \)

When you establish a synthetic long position with a strike price of \( \$50 \) against a current stock price of \( \$100 \), you’re effectively securing a future purchase at a net price of \( \$93.04 \). This is comprised of the strike price plus an upfront cost of \( \$43.04 \), netting you a tidy 7% discount from the stock’s current market value.

Now, about that \( \$1 \) dividend — in a conventional stock holding, this would be a modest income. Within our synthetic setup, however, it’s a different story. This dividend isn’t a bonus; it’s baked into the initial cost. It doesn’t augment your position; rather, it’s an additional consideration in your cost calculation.

The initial investment of \( \$43.04 \) isn’t merely an arbitrary amount; it’s a deliberate commitment of capital at the outset, distinguishing this strategy from others that might not necessitate such an investment. This figure isn’t just symbolic; it’s the lever you’re pulling to potentially enter the stock at a discount. Unlike scenarios where your synthetic position may begin with a net credit or no upfront cost, in this case, the investment is a calculated move. It demonstrates an understanding that the dividend has been priced into the options, thereby increasing your initial outlay in comparison to a hypothetical no-dividend scenario.

Here’s a little secret: You don’t have to stick around with your options trade until it expires. You can bail out early and still come out ahead. Think of it like this: when you get into a synthetic trade, you’re looking at a discount right off the bat.

So let’s say you start with a sweet $5.38 discount for taking on the trade. Fast forward six months, and you’ve got different plans or you just want to cash out. Here’s what happens:

\((S – K) + K \cdot e^{r \cdot \frac{T}{2}} – S \cdot e^{q \cdot \frac{T}{2}} = 100 – 100 + 100 \cdot e^{0.05 \times 0.5} – 100 \cdot e^{0.10 \times 0.5} = -\$2.59\)

You crunch the numbers and find out that now, you only need to give back $2.59 from the discount you got when you started. This means you’ve still pocketed a bit of cash. In plain speak, you got a bigger discount at the beginning ($5.38), and over time that discount shrinks a bit ($2.59). But hey, the difference? That’s yours to keep. It’s like getting a rebate on something you bought on sale in the first place. You’re saving money up front, and you keep saving even if you duck out early. It’s a solid move for anyone looking to get the most bang for their buck. With synthetic positions, it’s not just about the price of the stock going up. It’s about making the system work for you, so you can walk away with a little extra in your pocket. Understanding and applying synthetic positions allows traders to strategically navigate the markets, securing stock positions at below-market rates without waiting for a dip.

How do I find cheap synthetics?

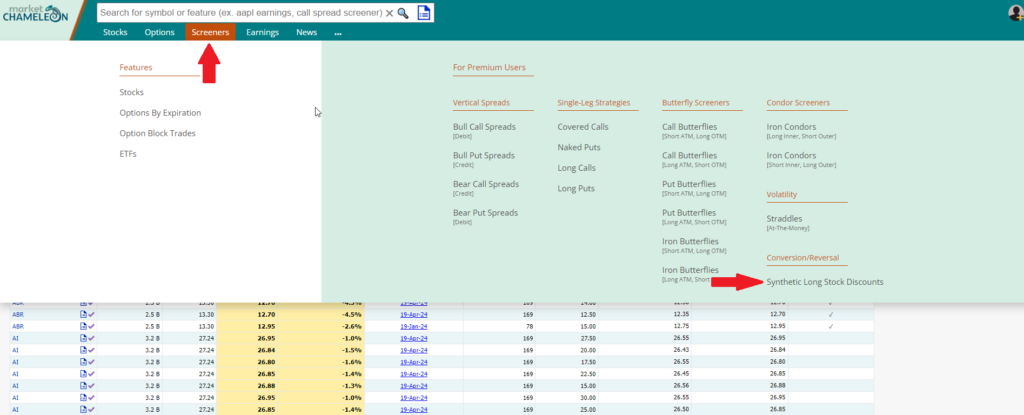

So, you’re probably wondering how to spot these cost-effective options among the myriad of expiration dates, stocks, and strike prices. This is where Market Chameleon steps in. For those with a pro account, it’s a game-changer. Simply log in and head over to the ‘Synthetic Long Stock Discount’ page, which you’ll find under the ‘Screeners’ section – the image below will guide you. It’s straightforward and efficient, almost like following a clear map to hidden discounts.

This platform is a haven for astute traders aiming to identify and seize top deals that could lead to significant savings. When you embrace synthetic positions, you’re not just riding the stock market roller coaster – you’re crafting a smart strategy to pad your wallet, ensuring you come out ahead. It’s practical, it’s clever, and ultimately, it can be more rewarding. That’s the smarter way to trade.

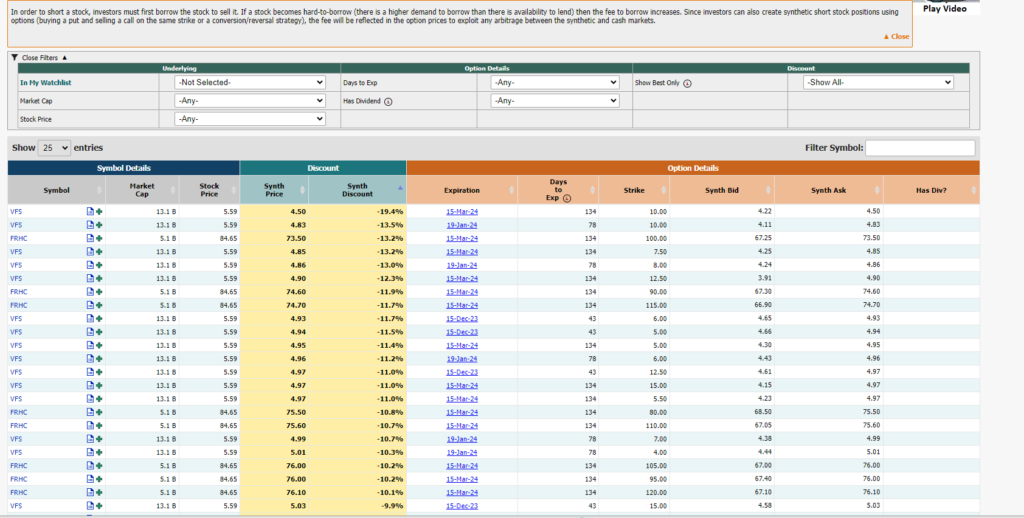

Once you land on the Synthetic Long Stock Discount page, you’re presented with a treasure trove of thousands of potential trades (as seen in the image below). Here’s how to pinpoint the best possible deal: The top menu is your command center, where you can tailor your search to fit your needs. Set your sights on a specific watchlist, filter by minimum market cap for targeting larger companies, or define the stock price range that suits your strategy. You can also adjust the days to expiry to match how long you’re willing to have your money in play and even opt to include or exclude stocks with dividends.

As you set your parameters, a comprehensive table springs to life below, detailing the statistics for each opportunity. Think of each row as a unique blend of stock, expiry, and strike price—forming a distinct trading opportunity. And remember, the table conservatively estimates your potential discount assuming you take the offer price in the synthetic position. However, savvy traders often do better, nabbing a price just above the midmarket, which could sweeten the discount even more.

Want to cut straight to the chase? Simply click on the ‘Synth Discount’ column to sort the opportunities. This lets you immediately zoom in on the most lucrative deals. It’s a streamlined process that sets you up to identify and act on some of the best opportunities in the options market.”

Note that the column “Has Div” is also very important, as it checks the dividend yield, which is part of the synthetic discount. So the effective discount would be the value in the column “synth discount” minus the dividend up to that expiry to get a fair comparison.